What is the current situation?

Bounce back loans continue to make headlines months after they first became eligible to be repaid by the numerous genuine borrowers who took them out during the pandemic and subsequent lockdowns.

Sadly, these aren’t stories about how they’re being repaid in record numbers – in fact it’s quite the opposite with the most incredible story being the case against Tarek Namouz.

Namouz is a former pub landlord currently on remand and charged with eight counts of funding terrorist organisations in the Middle East. The prosecution alleges that Namouz “sent the proceeds of his coronavirus bounce back loans funding to Isis.”

The trial is set for November 21st and is only the latest in a series of negative stories about the failure to recoup billions of pounds of bounce back loans issued during the pandemic.

This follows publication of the latest Public Accounts Committee (PAC) report that said the government was “complacent in preventing fraud” against the bounce back loan scheme and estimated that it will lose almost £5 billion to fraudulent claims.

The committee noted that the scheme was delivered at “breakneck speed” which saw the government ultimately take 100% of the default risk but that as a result of this haste the necessary checks to stop widespread fraud were not implemented.

The scheme did not require lenders to make additional checks against a business’ claims including its stated turnover or even how long the business had been in existence.

Figures from the Department of Business, Energy and Industrial Strategy (BEIS) estimate that £17 billion of bounce back loans are unlikely to be repaid with £4.9 billion (29%) lost to fraud.

Earlier this year, Lord Agnew resigned from his post as efficiency minister calling the inability to stop Covid fraud as “one of the most colossal cock-ups in recent government management.”

PAC chair, Meg Hillier MP, said: “More than two years on, BEIS has no long term plans to chase overdue debt and is not focussed on lower level fraudsters who may well just walk away with billions of taxpayers’ money.

“The committee was unpleasantly surprised to find how little the government learned from the 2008 banking crisis and even now are not at all confident that these hard lessons will be embedded for future emergencies.

“BEIS must commit now to identifying what anti-fraud measures are needed at the start of any new emergency scheme so the taxpayer is better protected in future. It also needs to set out the trade-offs and what level of fraud it will tolerate at the outset.”

A Taxpayer Protection Task Force was launched late last year to try and recoup funds and the public pronouncements of the PAC will force HMRC and lenders to take an even tougher response to recouping as much outstanding bounce back loan debt as possible in 2022 and beyond.

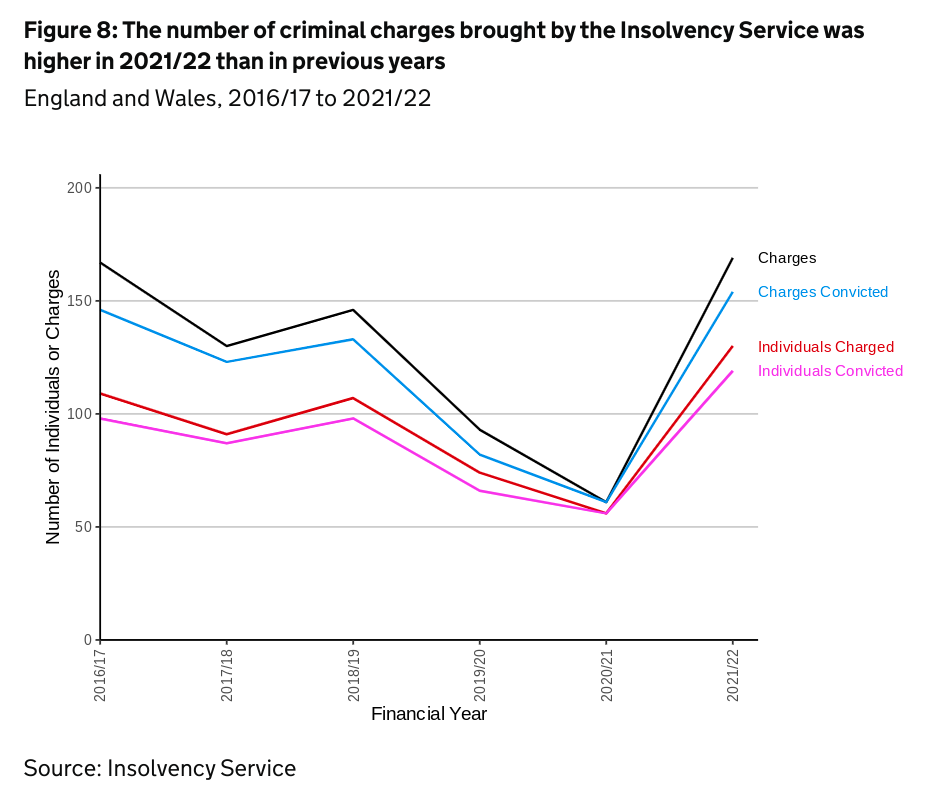

The report was published at the same time as the Insolvency Service reported on their own enforcement outcomes for the previous year to give some comparison on which departments are being most effective in enforcing the rules.

During 2021/22 the Insolvency Service reported that they had achieved the following:

- 130 individuals faced criminal charges brought by the insolvency service which secured 119 convictions

- 424 separate sentences were imposed based on these charges with sentences ranging from imprisonment to community orders of unpaid work, curfews and extended periods of supervision

- 802 director disqualifications with an average disqualification length of 5 years and 10 months

- Of these, 141 (17%) related to abuse of Covid-19 financial support schemes

- Wound up 52 companies in the public interest

- 6,500 former directors were still serving active disqualifications

Chris Horner, Insolvency Director with BusinessRescueExpert, said: “We’ve previously said that 2022 could be a year of crackdowns on bounce back loan borrowers and every story reminding the public just how much has been lent out and might potentially be lost makes it more likely.

“As well as increased powers for the Insolvency Service to investigate directors of dissolved companies, lenders will come under increased pressure from above to look to recoup any outstanding bounce back loan debt from borrowers and might put additional pressure on borrowers who have done everything right in obtaining and servicing the loan.

“A lot of otherwise viable businesses with bounce back loans may still have to close in future and with this increasing focus on the debts, they need to have the clearest understanding of their options than before.

“There are legal ways for businesses to close even if they have outstanding bounce back loan borrowing through a creditors voluntary liquidation (CVL) for example, but the best thing to do if there is any doubt or confusion would be to get some professional advice right now before the situation changes.”

One thing business owners and directors might have forgotten during the past couple of years is how quickly things can move or turn around.

Current circumstances might be very favourable but what happens if they change very quickly? It’s probable that no business owner in Kyiv had the current situation in their business plan for the year ahead.

While events as drastic as a pandemic or a war are unlikely, the fact that they’ve just happened and the ramifications are still being felt should focus every director’s thoughts to their business’ short and medium term future, no matter where they are or what they do.

And what is the best place to start?

How about a free consultation with one of our team of experienced experts who, once they get a clearer picture of your business, can let you know what options you’ve got to improve your situation.

Then you can effectively and efficiently begin to implement any suggestions to make sure that your business can survive and prosper beyond the next totally unexpected event.