More than 80% of CCJs issued remain unsatisfied

Our friends at The Registry Trust do a tremendous job of keeping track of all the County Court Judgements (CCJs) issued against individuals and businesses in the UK, Ireland and the Channel Islands.

They’ve now released the final official commercial CCJ statistics for 2025 and they have an interesting if worrying story to tell.

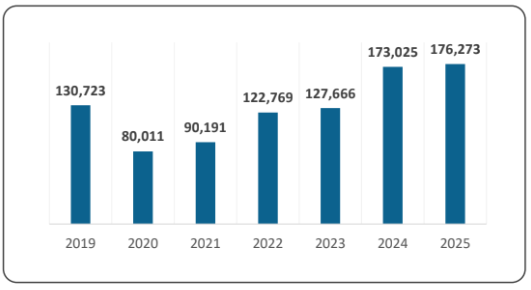

There were 176,273 commercial CCJs issued last year – the highest annual total for over seven years.

To give some additional context, this is 15% of the total of all CCJs issued last year – the vast majority being issued against individuals.

All statistics and graphics from The Registry Trust.

While this is a modest yearly increase from the total seen in 2024, it’s nearly double the total seen in 2021 and is another steep increase from 2022 and 2023.

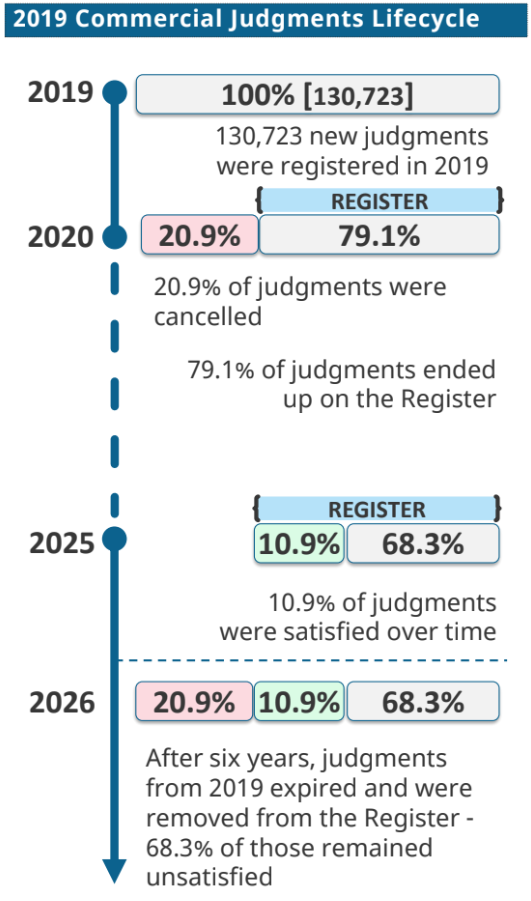

An example of how serious a CCJ being awarded against a business is – only 5.2% of all CCJs were satisfied (paid off in full) in 2025. An additional 14.1% were cancelled for various reasons but this still left more than four in five (80.7%) remaining unsatisfied and active on that company’s credit file for up to six years from the date of issue.

The trend is not good – This is the lowest number of satisfied cases in seven years and has gone down by 50% annually and is the highest number of unsatisfied cases over the same period (up 12% on last year).

Clearly more companies are finding it increasingly difficult to clear a CCJ when they receive one than ever before.

The value of CCJs is also increasing

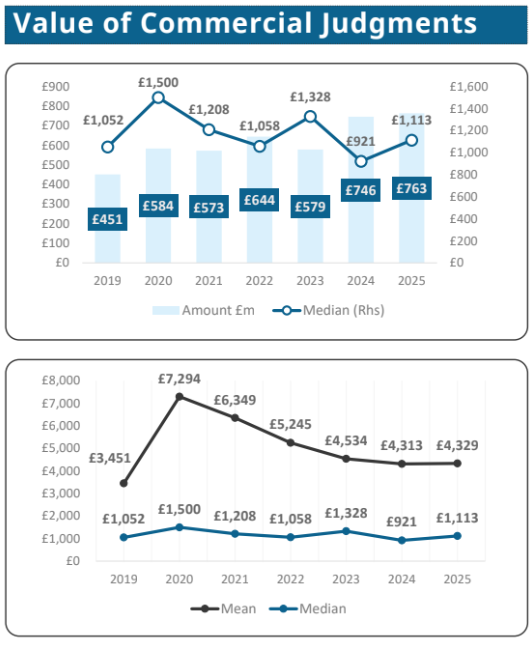

The annual commercial judgement activity shows a clear upward trajectory in overall value of a CCJ.

The median judgement value remains relatively stable, fluctuating between £921 and £1,500.

This shows that the typical case size hasn’t materially shifted and the core distribution of commercial judgements remains relatively consistent year on year. The occasional high-value case will skew the average but doesn’t reflect the broader market behaviour.

The median commercial judgement in 2025 was £1,115, rising from £921 the year before.

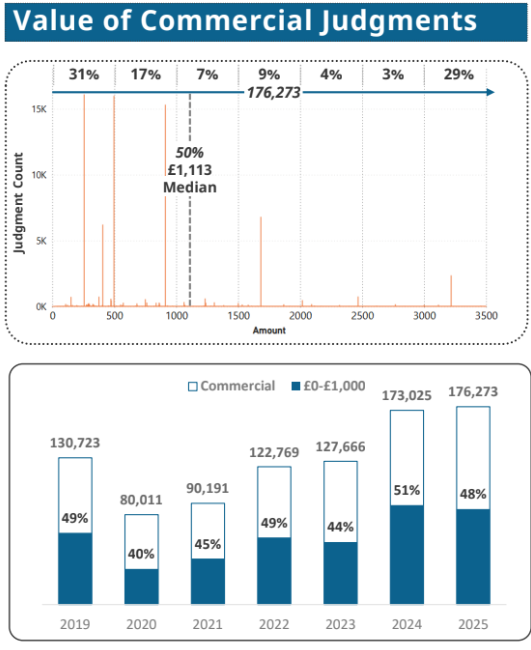

48% of all total judgements were for amounts of £1,000 or lower with the next most frequent values being for amounts of £3,000 or higher.

The real risks of a CCJ

Every company that receives a CCJ is already at a higher risk of insolvency than other businesses but sole traders are in even more jeopardy than that.

Limited companies enjoy specific legal protections when it comes to their business debts which aren’t shared by sole traders.

If they receive a CCJ then they would be expected to settle any outstanding debts from their own personal assets or accounts. Remember, a CCJ is not like a winding-up petition, which has legal standing to compel companies to repay their debts.

Instead it gives High Court Enforcement Officers (HCEOs) and bailiffs the legal right to visit business premises (including the home of a sole trader if they are one and the same) and seize company assets up to the value of any outstanding debts.

Any CCJ is also publicly available for view on the Register of Judgements, Orders and Fines so any creditor, customer or supplier can find it.

This will make future borrowing more expensive and difficult to obtain as an unpaid CCJ remains on a business’s credit file for six years.

Chris Horner, insolvency director with BusinessRescueExpert, said: “It doesn’t necessarily mean that a business receiving a CCJ will automatically go into insolvency but the data and ongoing trends show that it’s a distinct probability.

“It doesn’t get any more stark than realising that 80% of CCJs remain unsatisfied.

“Given our experience over 21 years, we’d agree with this assessment and stress to any director or business owner that if they or their business receives a CCJ then they should get in touch as soon as they can.

“They may have more options than they think, depending on their individual circumstances, and we’ll probably be able to work with them to create an effective roadmap to a sustainable and brighter future for them and their business.”