End of the financial year rush sees Administrations rise over 82% annually

While we were all hoping that the economic and energy turmoil unleashed in the Middle East would have abated by now, the latest corporate insolvency figures for March 2026 show the real-world effects they had.

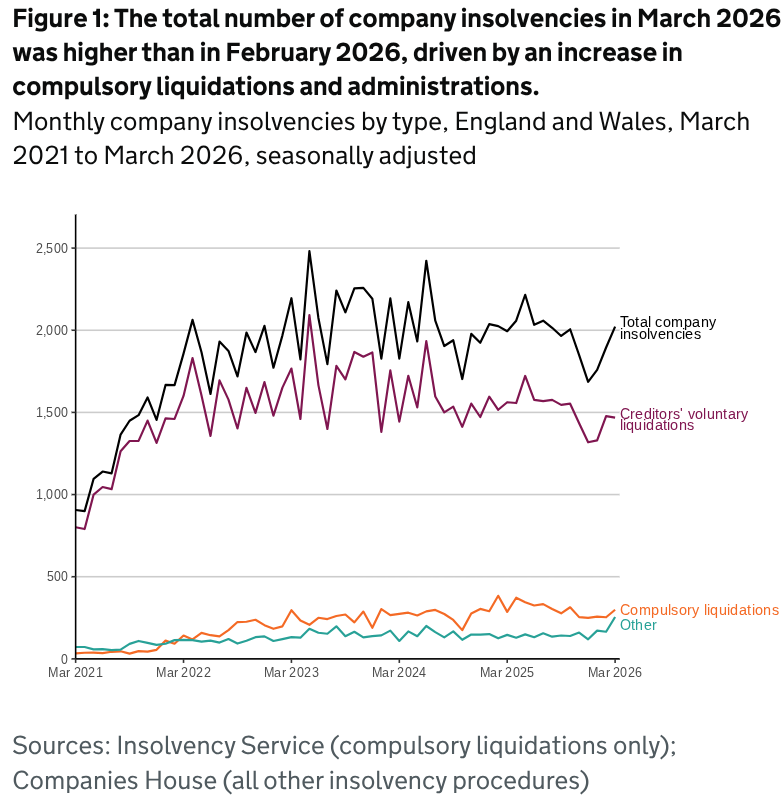

The Insolvency Service confirmed that there were 2,022 registered company insolvencies recorded last month in England and Wales, which was 7% higher than the 1,878 recorded in February and 1% higher than in the same month last year (1,995).

The figures for March complete the first financial quarter of the year and while the number of business insolvencies from the end of 2025 to the end of February were lower than the levels seen in the previous four years, the large increase this month brings them into line with the 2025 average level.

Analysis

Creditors Voluntary Liquidations (CVLs)

Of the 2,022 corporate insolvencies in March, the most frequent category remained Creditors’ Voluntary Liquidations (CVLs) with 1,468. Curiously, this is both 6% lower than the same month a year ago and 1% lower than last month.

CVLs accounted for 73% of all company insolvencies in March – a monthly fall of 5%. The average number of CVLs over the last five months has been 9% lower than the average monthly number in 2025.

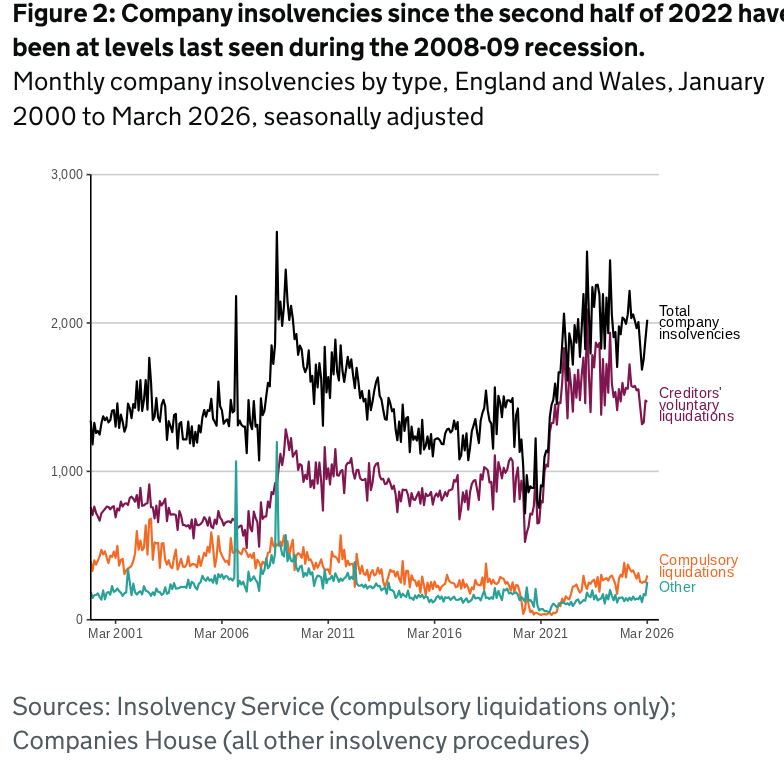

In 2025, CVL volumes slightly decreased by 2% from 2024 and by 10% from the record-highs of 2023. The past four years have seen the highest four numbers of CVLs since recording began in 1960. Between 2017 and 2019, CVLs had been rising at approximately 10% per year but during the pandemic they fell to their lowest levels since 2007.

Compulsory Liquidations

There were 299 compulsory liquidations in March 2026 which was 18% higher than last month’s total and 4% higher than in March 2025. They are still 4% lower than the 2025 monthly average.

In 2025, compulsory liquidations were at their highest levels since 2012 having increased by 15% from 2024. This continued to increase from record low levels seen in 2020 and 2021 when restrictions were applied to the use of statutory demands and winding-up petitions (leading to compulsory liquidations).

HMRC will continue to target companies that owe outstanding Corporation Tax, VAT, PAYE or National Insurance Contributions (NICs) arrears this year. More agents are being recruited, more funding has been allocated and they will use it to retrieve as much as possible from debtors.

Administrations

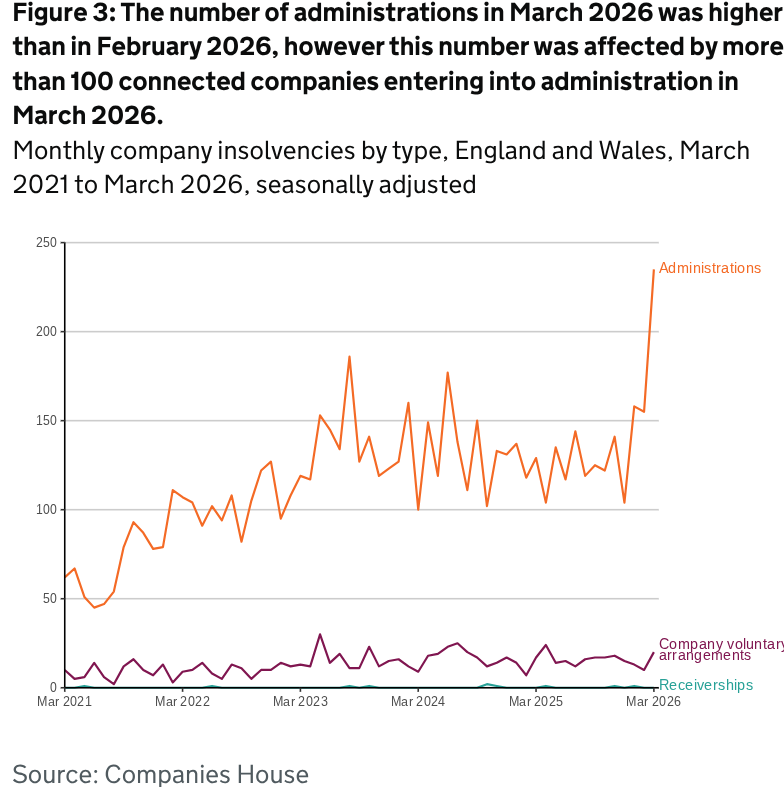

There were 235 administrations in March which was 52% higher than the previous monthly total and 82% higher than in March 2025.

More than 100 connected companies in the Real Estate sector entered administration in March so this increase might be a large one-off event rather than reflecting the underlying trend in administration numbers.

In 2025 as a whole, the number of administrations decreased by 8% from 2024. This followed a sustained increase between 2022 and 2024 after the 18-year annual low seen during the Covid-19 pandemic in 2021.

Company Voluntary Arrangements (CVAs)

There were 20 Company Voluntary Arrangements (CVAs) in March which was the highest monthly total for a year. It was double (100%) the total from a month previously and 18% higher than in March 2025.

CVA numbers continue to remain low compared to their historic levels.

There were no receivership appointments in March 2026. Receivership appointments are now rare, with only three being registered in the past 12 months ending in March.

There were no moratoriums or restructuring plans registered at Companies House in March 2026. Between June 26 2020 and March 31 2026, 68 companies obtained a moratorium and 57 companies had a restructuring plan registered at Companies House. Both procedures were created by the Corporate Insolvency and Governance Act 2020.

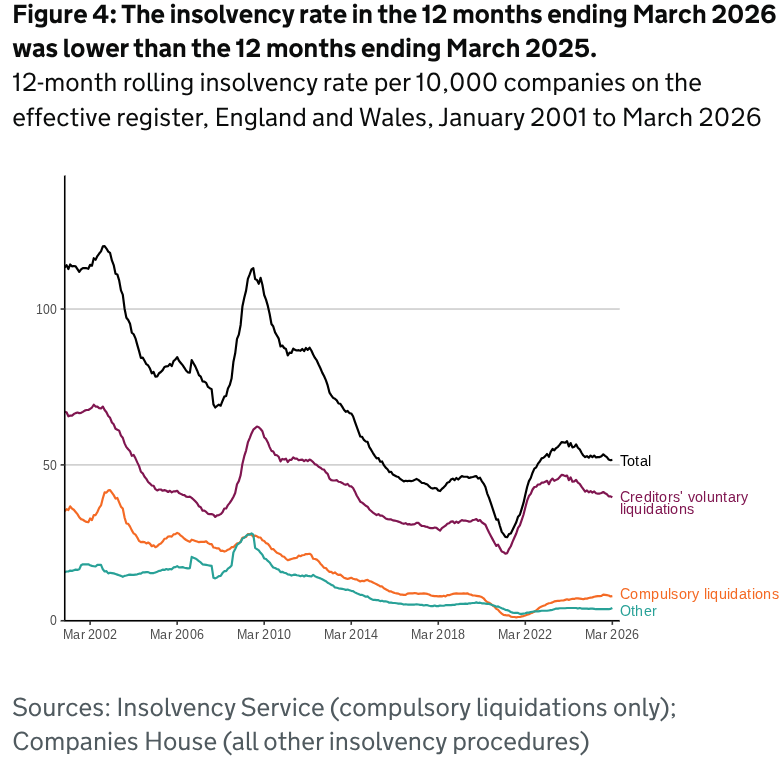

The rolling company insolvency rate in the last 12 months was 51.6 per 10,000 companies on the effective register in England and Wales. This corresponds to one in 194 companies entering insolvency – the same ratio as last month.

Insolvency rates are calculated as a proportion of the total number of companies on the effective register and are more comparable over longer time periods than the absolute numbers. A 12-month rolling rate is presented to reduce the volatility associated with estimates based on single months. The March 2026 rates were calculated using data covering the period from April 1 2025 to March 31 2026.

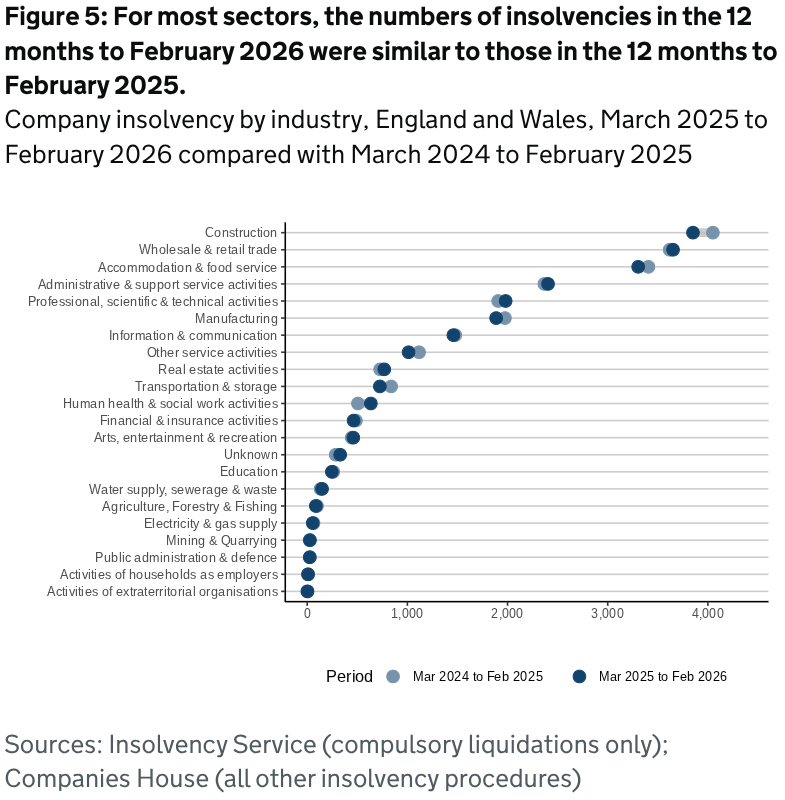

Companies by Standard Industrial Classification (SIC)

The six industries (in accordance with SIC 2007) that experienced the highest number of insolvencies in the 12 months to February 2026 were:-

- Construction (3,851 – 17% of cases with industry captured)

- Wholesale and retail trade; repair of motor vehicles and motorcycles (3,652 – 16% of cases with industry captured)

- Accomodation and food service activities (3,304 – 14% of cases with industry captured)

- Administrative and support service activities (2,404 – 10% of cases with industry captured)

- Professional, scientific and technical activities (1,981 – 9% of cases with industry captured)

- Manufacturing (1,886 – 8% of cases with industry captured)

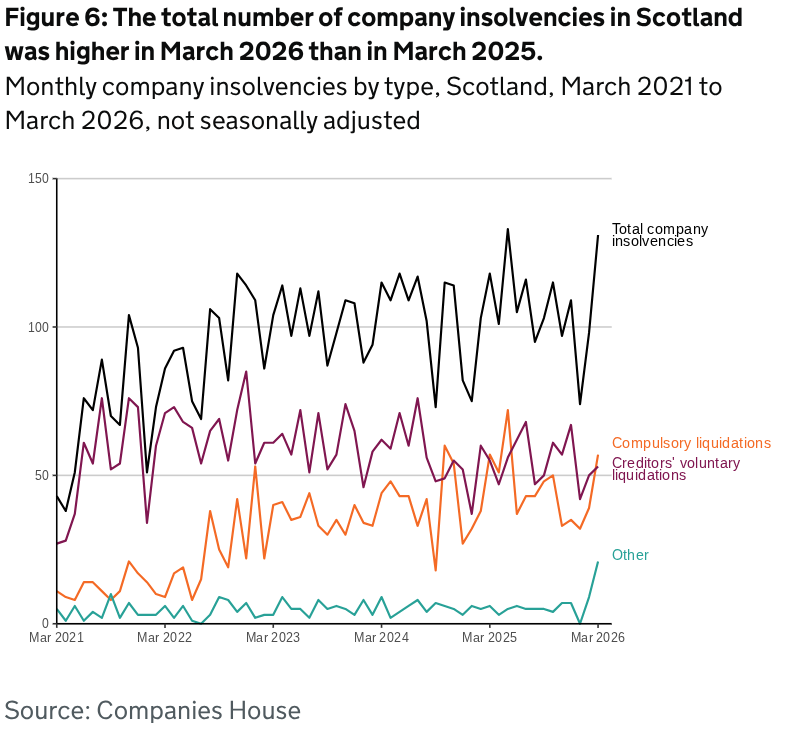

Scotland

In March there were 131 company insolvencies registered in Scotland which was 33 higher than last month and 11% higher than the same month a year previously.

The total number of company insolvencies was comprised of 53 CVLs (up from 50); 57 compulsory liquidations (up from 39); 18 administrations (up from six) and three receivership appointments (up from two). There were no CVAs.

Scotland’s insolvency regime is partly devolved.

The Accountant in Bankruptcy (AiB) is Scotland’s insolvency service and administers the Register of Insolvencies which is a publicly accessible statutory register regarding the insolvency of individuals and businesses in Scotland including company liquidations and receiverships.

Between June 26 2020 and March 31 2026, there were three restructuring plans and two moratoriums in Scotland.

Scotland has always traditionally recorded more compulsory liquidations than any other kind of insolvency procedure but they were overtaken by CVLs in April 2020 and typically remained higher until a three month period from March to June 2025 and again this month.

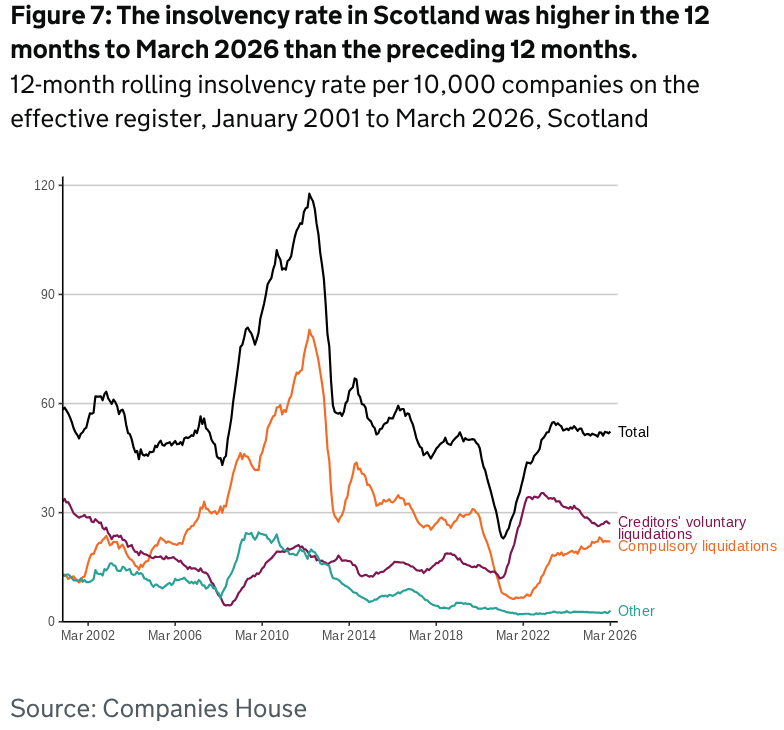

The total insolvency rate in Scotland in the 12 months to March 2026 was 52.3 per 10,000 companies on the effective register. This was up by 0.7 from the preceding 12 months ending March 2025.

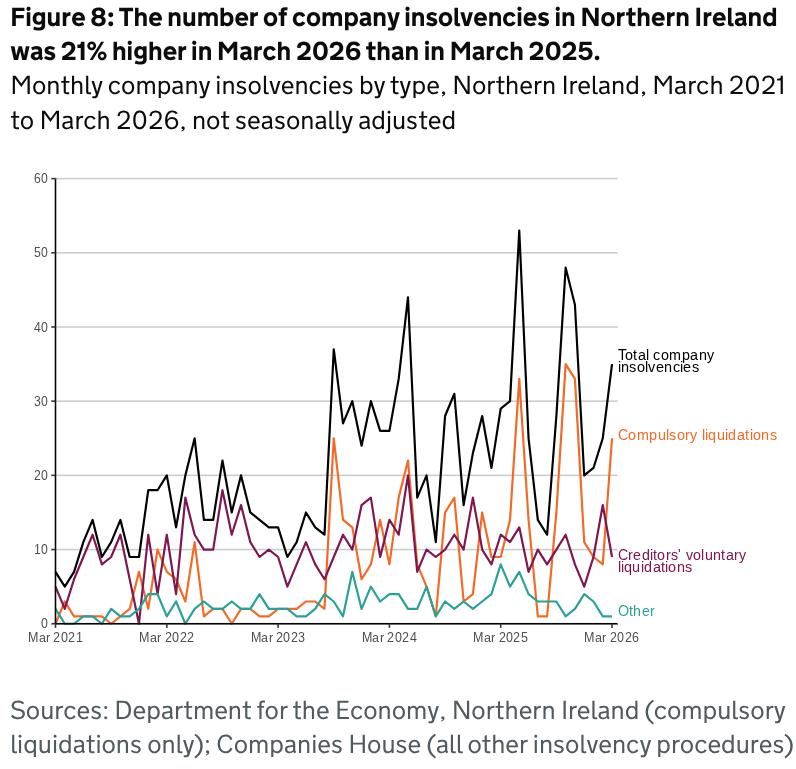

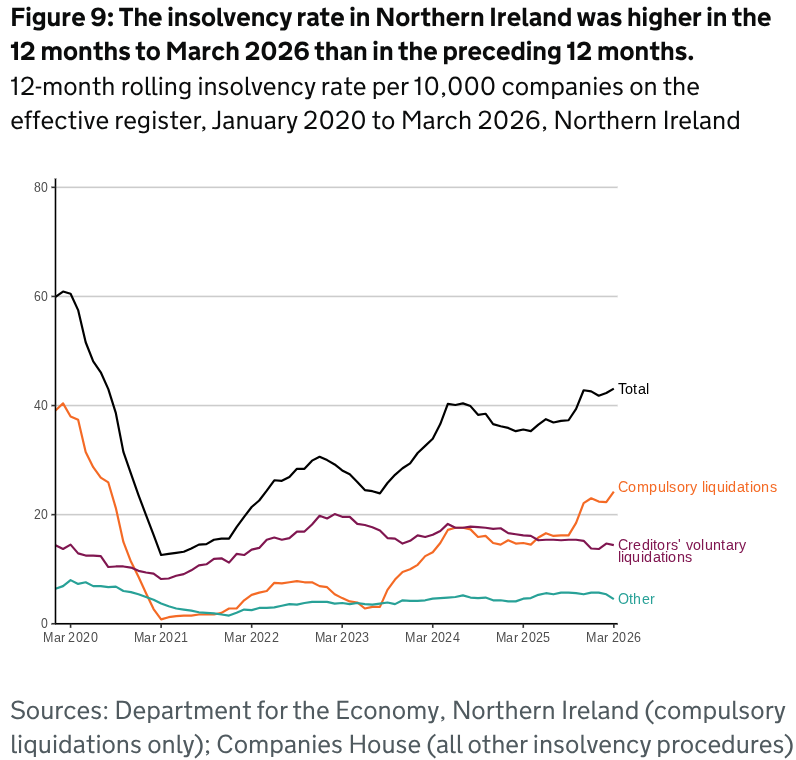

Northern Ireland

In March there were 35 company insolvencies in Northern Ireland, which was ten higher than last month and 21% higher than the same month a year previously. The total consisted of 25 compulsory liquidations (up from eight); nine CVLs (down from 16) and one CVA (up from zero). There were no administrations (down from one) or receivership appointments.

Between June 26 2020 and March 31 2026, there was one moratorium in Northern Ireland and no restructuring plans.

The total insolvency rate in the 12 months to March 2026 in Northern Ireland was 43.1 per 10,000 companies on the effective register. This was an increase of 7.5 from the 12 months to March 2025.

The total number of company insolvencies for the whole of the UK in March 2026 was 2,188 – a month-on-month increase of 187.

Tom Russell, president of R3, the UK’s restructuring, turnaround and insolvency trade body, said: “Corporate insolvencies increased by 7% in March, compared to the previous month, rising to 2,022 cases, although numbers were at similar levels to March 2025.

“Administrations were 52% higher than the previous month, in part explained by 100 connected companies entering administration in the Real Estate sector.

“Just as business and consumer confidence was starting to improve, the economic fallout from the Middle East conflict, in particular higher fuel and energy prices, are putting a financial squeeze on UK businesses and households alike.

“While it may be too early to see the full impact of the worsening economic situation in the formal insolvency statistics, energy and fuel costs have risen significantly and for many businesses, this has come at the same time as customers are becoming more cautious with their spending. That combination is extremely challenging, particularly for businesses with limited financial headroom.

“Manufacturers, particularly those companies with energy-intensive operations, have been hit hard by rising gas and electricity prices. Recent high-profile cases have highlighted these challenges, with well-known ceramics manufacturer, Denby Pottery, citing rising energy costs as a key factor in its decision to call in administrators.

“At this stage, businesses can no longer assume that conditions will quickly return to normal. Many will need to start putting contingency plans in place. Insolvency practitioners are increasingly expecting to see greater demand for professional support as businesses adjust to the reality of a more prolonged period of financial pressure.”

The events of the first months of 2026 show us that nothing can be taken for granted and that circumstances can change very quickly.

This is worth keeping in mind if your business hasn’t made the progress you wanted this year. There is still more than enough time to make the decisions and changes necessary to get to where you want to be – personally and professionally.

Get in touch with us for a free initial consultation about the options you could have to help you create and work through a feasible plan and strategy no matter what your short and medium term goals for the year.

We’ll help you to implement them – the sooner you get in touch, the sooner we can begin.