When you are looking forward to something arriving or happening, why does it always seem to take longer?

Due to the Easter break, last month’s official corporate insolvency statistics were delayed by seven days so it’s taken five weeks for them to be published. We know because we’ve been counting every single minute of them!

But the good news is that The Insolvency Service have now released their latest monthly insolvency statistics for businesses.

We’ll post an analysis of the Q1 figures later this week but right now we’re going to concentrate on March, the final month of the 2023/24

March’s official figures for company insolvencies in England and Wales saw a total of 1,815 recorded. This was 17% lower than the previous month’s total of 2,102 and 17% lower than the same month in 2023 (2,193) but it is still much higher than pandemic affected years of 2020 and 2021 as well as the pre-Covid years of 2014 to 2019.

Analysis

Of the 1,815 corporate insolvencies in February, Creditors Voluntary Liquidations (CVLs) remain the most frequent type of business insolvency with 1,437.

This was a reduction of 305 from last month (18%) and a 19% reduction from the same month a year ago. CVLs make up 79% of all corporate insolvencies, down 2% from the proportion seen last month.

There were 261 compulsory liquidations in March which was a slight decrease from the 268 recorded in February. This is also 9% lower than last March’s total.

The relatively high number of involuntary liquidations shows that creditors led by HMRC continue to be aggressive in their attempts to recoup outstanding assets from debtor companies.

The increasing use of winding up petitions and statutory demands indicates that they will continue to push and will force more and more directors into making serious decisions about the future of their companies.

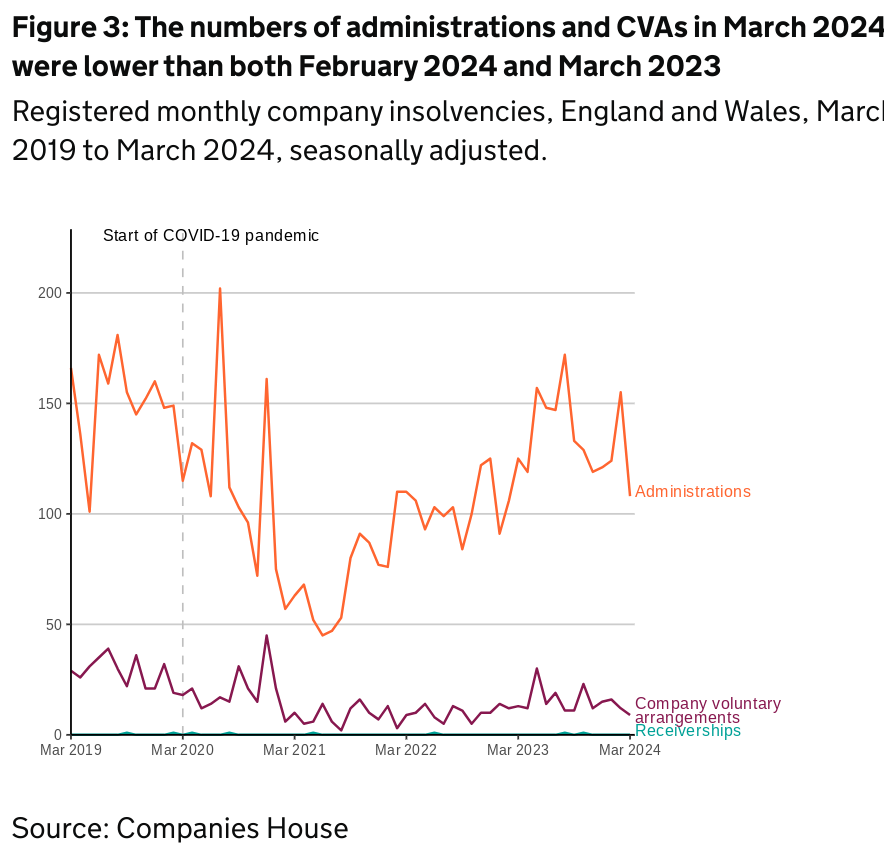

There were 108 administrations in March, a 30% reduction from the 155 seen in February and an annual decrease of 14% from the same month a year ago.

There were nine company voluntary arrangements (CVAs) last month. This was a decrease of three from February and was also three less than the total a year ago.

There were no receiverships registered last month nor moratoriums registered at Companies House but one restructuring plan was registered.

Between June 2020 and March 2024, 52 companies have obtained an insolvency moratorium and 23 companies have had their resturing plan registered.

Scotland

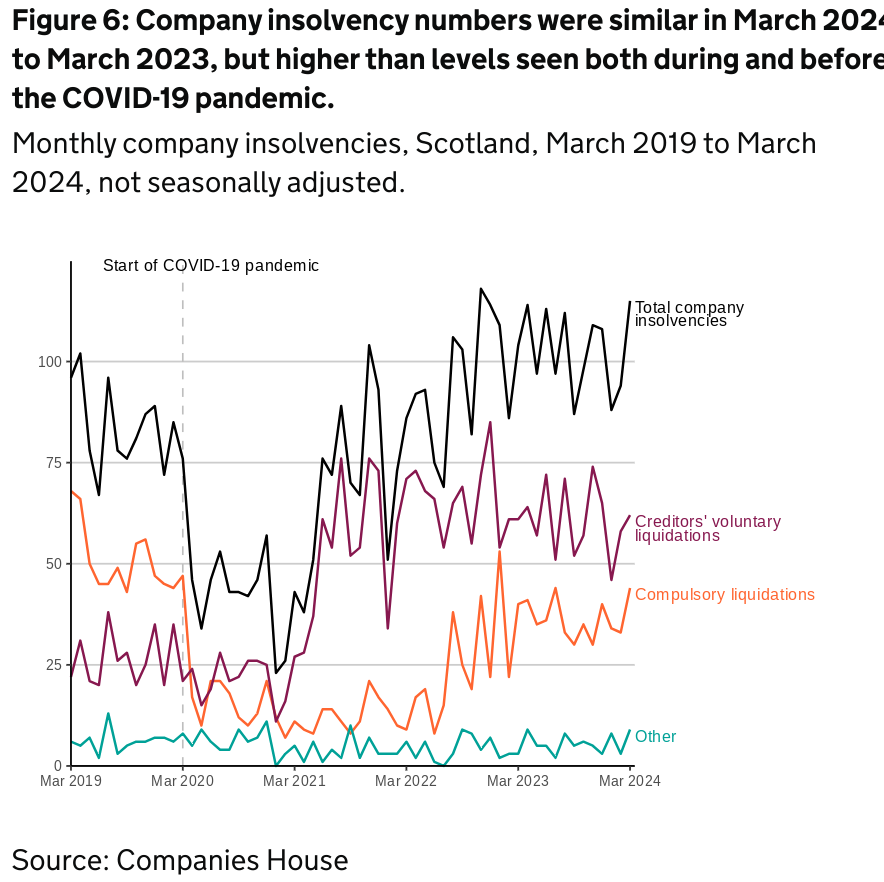

In Scotland last month there were 115 company insolvencies registered. This is 21 more than last month and 11% higher than the same month a year ago.

This month’s total consisted of 62 CVLs (up from 58); 44 compulsory liquidations (up from 33) and nine administrations (up from three). There were no CVAs or receivership appointments recorded.

Historically, compulsory liquidations had always been the most common type of company insolvency in Scotland but since the advent of Covid in April 2020, the numbers of CVLs matched then overtook them and have remained higher ever since.

This shows that Scottish directors and accountants have become more proactive in taking matters into their own hands when deciding the future of their businesses.

Northern Ireland

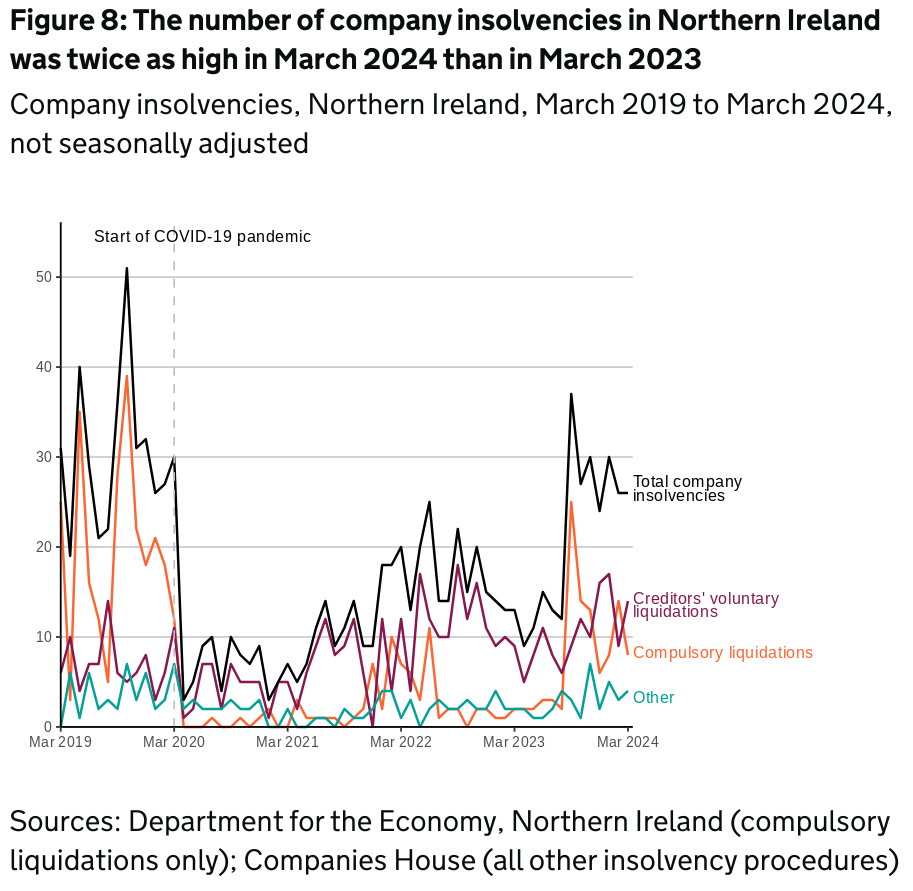

In March 2024, there were 26 company insolvencies registered in Northern Ireland, which was the same as the number recorded in February and was double the number recorded in March 2023.

This total consisted of 14 CVLs (up from nine); eight compulsory liquidations (down from 14); three CVAs (up from zero) and one administration (down from three). There were no receivership appointments recorded.

The total number of company insolvencies in the whole of the UK in March is 1,956 – a reduction of 266 from February.

Tim Cooper, the new President of R3, the insolvency and restructuring trade body said: “The biggest driver of the monthly and yearly fall in corporate insolvency numbers is a reduction in CVLs. However numbers for this process and overall levels of corporate insolvency are still higher than they were pre-pandemic.

“High costs and constrained spending have continued to hit businesses hard in the first three months of this year. The latest available sectoral data shows that construction is currently the industry experiencing the highest levels of insolvency, and the figures for this sector for November 2023 to January 2024 are slightly higher than they were for the same period last year.

“This is because insolvency numbers have increased amongst firms working on the construction of residential and non-residential buildings, as well as in specialist construction activities.

“I would suggest that the main drivers of this are the delays in construction starts in the three months to October of last year, which will have affected the main contractors and those specialist construction firms whose work takes place in the later stages of construction projects.

“These specialist firms are also vulnerable to impacts of delayed start times and of the cost of materials. There were also a number of high profile construction sector insolvencies in that period, and the cascade-effect can take a while to impact on the supply chain into this sector.

“While the wider trading climate is a challenging one, there are signs directors expect revenues to increase this year, and this suggests the mood among the business community is becoming more positive. However, it remains to be seen whether inflation falls quickly enough to benefit businesses, and whether the hoped-for increases in income outstrip potential rises in costs and wages.

“Directors need to be alert to the signs their business is distressed, and act on any indications it might be as soon as they present themselves.

“Cash Flow issues, increases in stock and problems paying taxes or invoices are all signs a business is financially distressed, and the quicker these are acted upon and professional advice sought, the greater chance there is of the situation improving.”

While the 2023/24 financial year ended with some positive news with a reduction in corporate insolvencies, the beginning of 2024/25 might tell a different story as several new financial measures appear to bite businesses.

Higher staff wages, interest rates stuck at decade long highs, inflation still above the Bank of England’s target rate and business rates increasing are just some of the macro issues that every business is having to contend with.

Throw in sector and area specific issues and it could be that the next 12 months are getting off to the bumpiest start and directors need a steady hand to help settle things down.

This is why it is so important to get some professional, important advice and why we continue to offer a free initial consultation for any business owner or director that requires one.

Once they get a better understanding of the options available to them, they will be able to implement the key decisions to help achieve their goals in the rest of 2024 and beyond – but only if they make the key call – and get in touch first.