But could there be better news for the rest of 2024?

April 2013 saw all BBC television services leave Television Centre and move to Broadcasting House in the centre of London. Lady Thatcher’s funeral was watched by millions on those channels; “Get Lucky” was released by Daft Punk and would hit number one all over the world within weeks and two bombs exploded near the finish line of the Boston marathon.

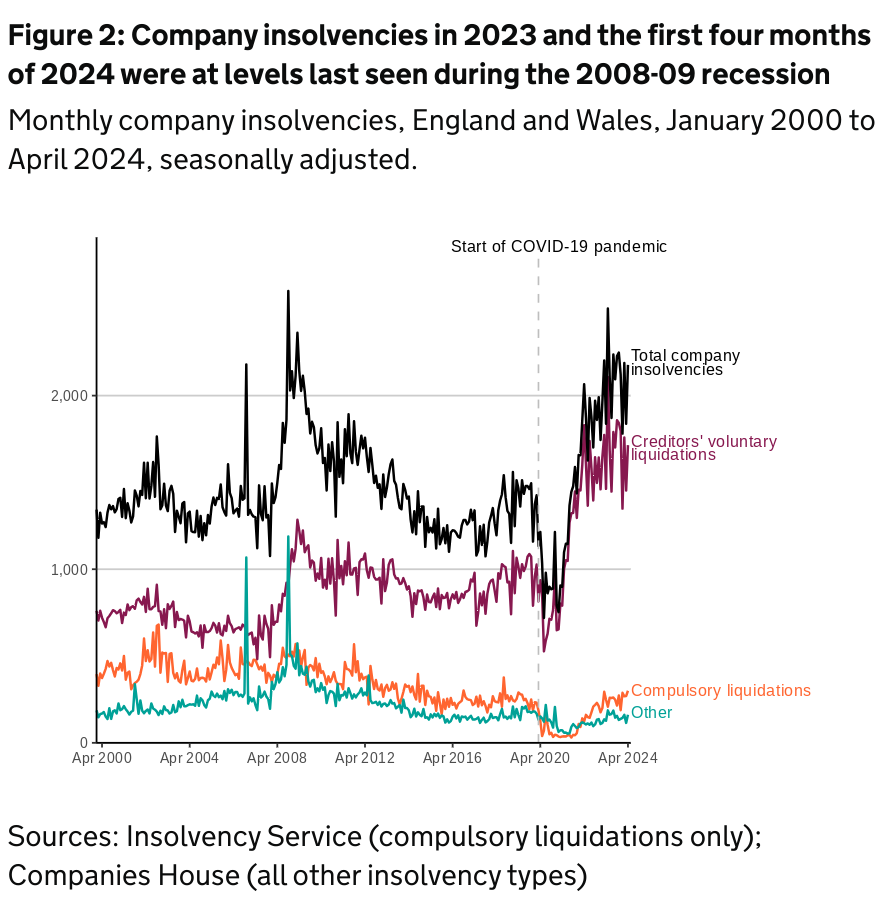

This was also the last time when insolvency figures for April would be higher than the total released by the Insolvency Service in their latest corporate insolvency statistics bulletin.

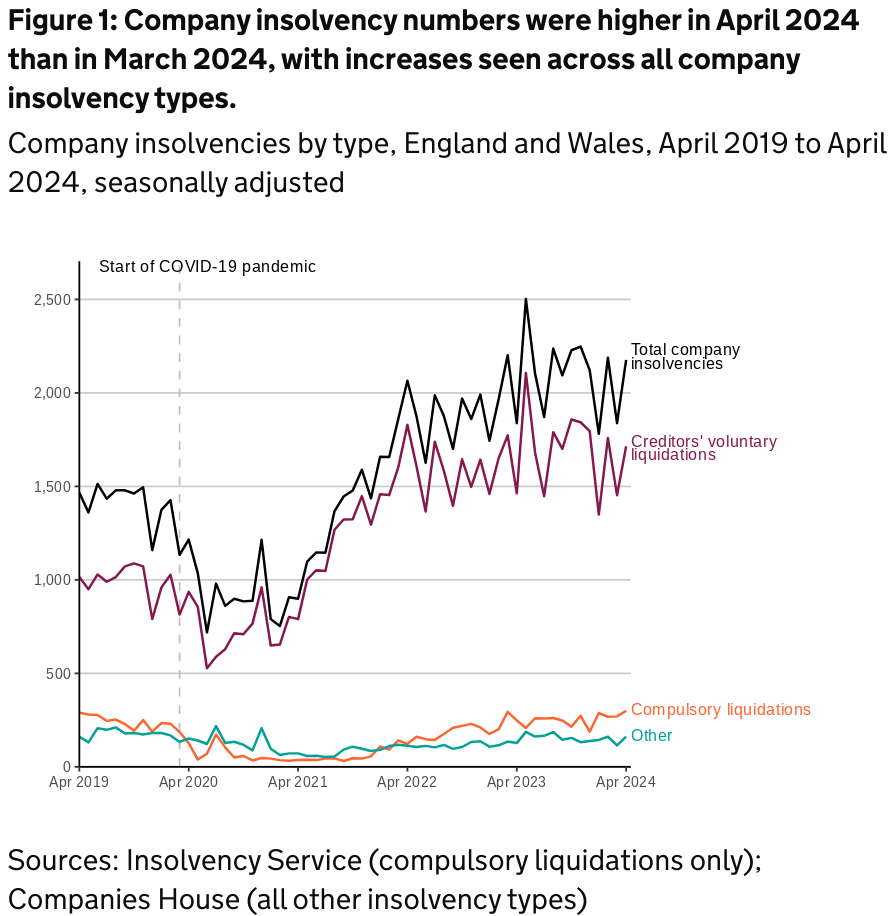

The official figures for company insolvencies in England and Wales in April saw a total of 2,177 recorded.

This total is 18% higher than the previous month’s total of 1,815 and also 18% higher than the same month in 2023 (1,838). This is also the highest number recorded in April since 2013.

So what is driving these unusually high numbers and what clues can it give us to what else lies ahead this year? Read on to find out!

Analysis

Of the 2,177 corporate insolvencies in April this year, Creditors Voluntary Liquidations (CVLs) remain the most frequent type of business insolvency with 1,715.

This was an increase of 262 from last month (18%) and a 17% increase from the same month a year ago. CVLs make up 79% of all corporate insolvencies, which is the same proportion as last month.

There were 300 compulsory liquidations in April which was an increase of 30 from the 270 recorded last month. This was a 11% increase and a 21% increase on the total from April 2023. This is also the highest monthly total recorded for seven years and shows that HMRC and other creditors are being more aggressive in their attempts to recoup outstanding debts.

This is underlined by the increase in the use of statutory demands and winding up petitions which will continue to force more directors to make serious decisions about the future of their businesses.

There were 144 administrations in April, a 36% increase from the 106 seen in March and an annual increase of 25% from the same month a year ago.

There were 18 company voluntary arrangements (CVAs) last month. This is double the total from last month and is 50% higher than the total from April 2023.

There were no receiverships registered last month in England and Wales nor were there any insolvency moratoriums or restructuring plans registered with Companies House.

Between June 2020 and April 2024, 52 companies have obtained an insolvency moratorium and 23 businesses have had their restructuring plan registered with a court.

Scotland

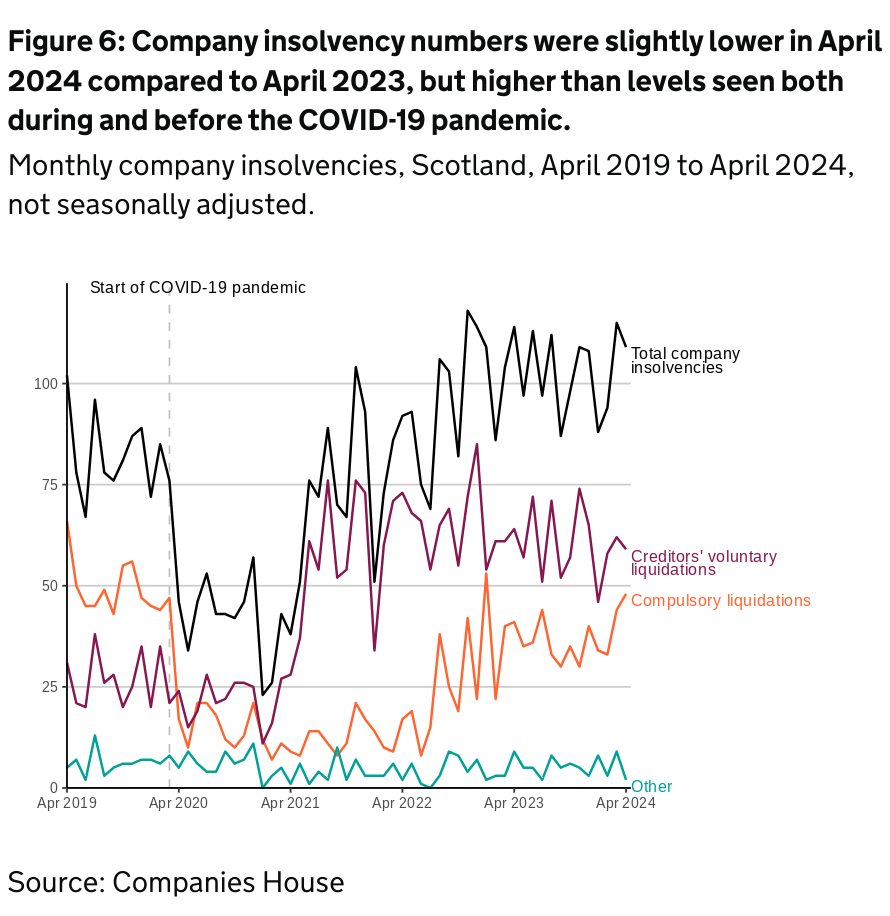

In Scotland last month there were 109 company insolvencies registered in Scotland. This was six fewer than last month and was also down 4% on the number seen in April 2024.

The total consisted of 48 compulsory liquidations (up from 44); 59 CVLs (down from 62) and two administrations (down from nine). There were no CVAs or receivership appointments.

In Scotland compulsory liquidations have historically been the most frequent type of company insolvency but since April 2020, the number of CVLs have become the most common type.

This underlines how proactive Scottish directors and accountants have become in seizing the initiative and making their own decisions on the future of their businesses before creditors and the courts decide to.

Northern Ireland

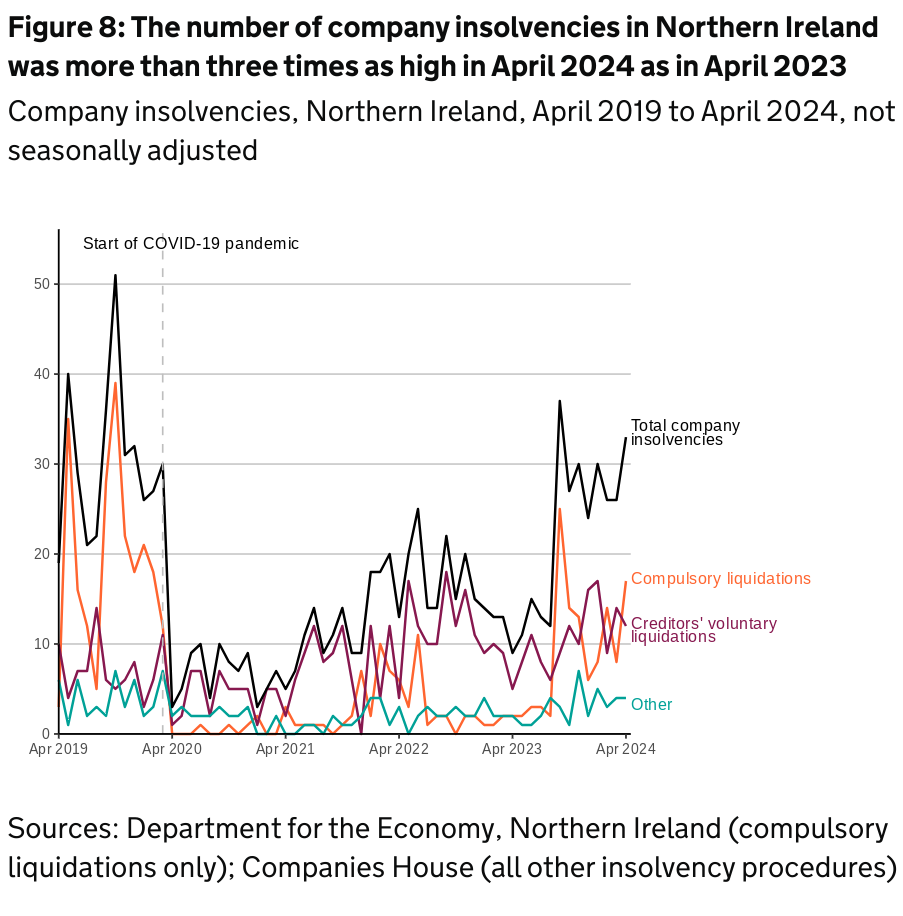

In April 2024 there were 33 company insolvencies registered in Northern Ireland. This was six higher than last month but more than three times (267%) the number recorded in April 2023.

The total consisted of 12 CVLs (down from 14); 17 compulsory liquidations (up from eight); two CVAs (down from three); and two administrations (up from one). There were no receivership appointments recorded last month.

The total number of company insolvencies in the whole of the UK in April is 2,319 – an increase of 363 from last month.

“Insolvencies have reached a level not seen since the previous recession in 2008”

Tim Cooper, the new President of R3, the insolvency and restructuring trade body said: “The last year and the last quarter have seen corporate insolvency numbers reach a level not seen since the previous recession in 2008/09.

“The fact the UK had entered a recession (albeit relatively modest) during the last two quarters of 2023 was a contributing factor, however the recession would appear to have been short lived with a better than expected growth in GDP of 0.6% between January and March which has largely cancelled out the recession itself.

“Against this backdrop, inflation is falling and the Bank of England have held interest rates for a further month, with market speculation abundant as to whether and when a cut is on the cards. Corporate registrations are at a record high, so there are factors at play which suggest some return of business confidence, if not consumer confidence with cost-of-living pressures still playing their part. Working out what is going on is therefore becoming more nuanced than simply blaming the pandemic, cost of living, inflation and interest rates.

“The annual and monthly increases in corporate insolvencies shown in the figures have been driven by an increase in all types of corporate insolvency process, but the key areas which stand out are the increases in CVLs, most of which relate to small and medium sized companies, which has seen the largest rise after a brief decline in March and administrations.

“One factor in the increase in CVLs is likely to be down to directors closing their business at the end of the financial year – either because they believe the market won’t improve or because they’ve simply had enough after four tough years.

Another possibility could be difficulties in small businesses in distress being able to access more complex and more expensive forms of restructuring, and having to resort to liquidation as a means of dealing with unserviceable debt.

“While the increase in administrations isn’t by a large number, it does suggest that there are an increasing volume of businesses that could potentially be rescued rather than wound-up and as the economy recovers we would anticipate this rise will continue.

“We’ll need to keep a close eye on this, as the trendline is upwards and the causes are not clear against a backdrop of an apparent increase in business confidence and the so-called “green shoots” of economic recovery. One would expect liquidations to level out or decline, as rescue mechanisms begin to replace closures – but we shall have to wait and see.

“The sectoral data we have available shows that the construction, retail and hospitality sectors continue to experience the highest insolvencies this year so far.

“Retail and hospitality businesses have been especially affected by consumers’ wariness about spending money, poor weather in February and a tough pre-Christmas trading period. Issues with the weather will also have affected the construction industry, as will the fall in new work it has suffered from since the start of the year.

“Despite the difficult business climate over the period these figures cover, there is some cause for optimism.

“The economy is growing again and business and consumer confidence are both improving, and while businesses remain concerned about costs and consumer demand, the mood is generally more positive with a significant increase in new company registrations being reported by Companies House.”

The 2023/24 financial year ended with a reduction in corporate insolvencies but 2024/25 has begun with a bang – and unfortunately it’s in the wrong direction.

Despite some optimism the same macro issues exist for directors and business owners to overcome.

Facing higher staff wages, interest rates at decade-long highs, inflation above the Bank of England’s target rate, business rates increasing and the sector and location specific issues that each business has to deal with and you can see how any positive general economic vibes are being drowned out by the actuality of day to day trading.

This is why it is critically important to get the best impartial professional advice and why we continue to offer a free initial consultation to any director who would like to arrange one.

Once they understand all the options available to them based on their own unique circumstances, they will be better placed to implement the key decisions that need to be taken now to give them the best chance to making the changes needed to achieve their goals and targets in 2024 and beyond – but only if they get in touch with us first.